After the Bitcoin, the bilur is a new private money backed by oil. Despite its physical roots (one millions barrels under Texas) this money does not offer a stronger value than standard cash. The will to anchor money in a physical foundation (gold, oil, other) is common, but in the end money is by definition a bubble (not a speculative one, be reassured).

Oil does not really preserver value

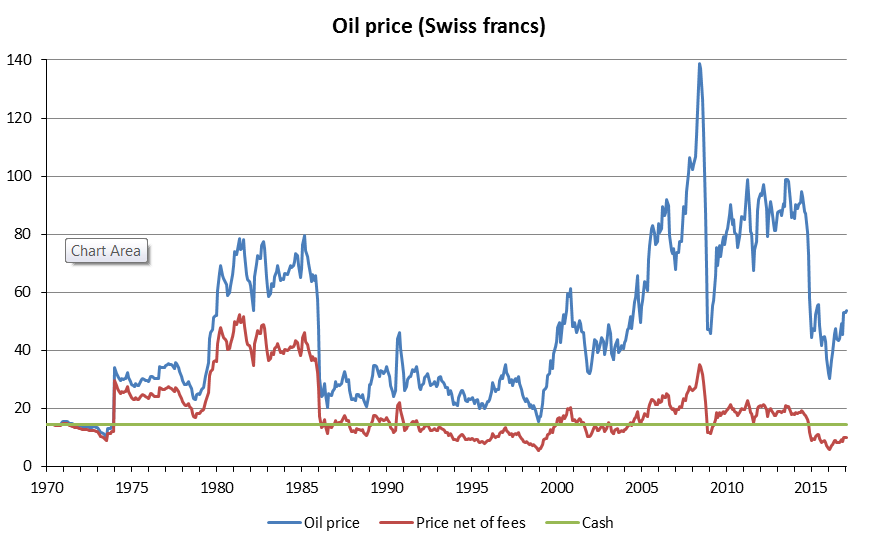

At first glance a physically backed currency is a good way to preserve the value of one’s savings. In fact not really. The figure below shows the oil price since 1970 (in Swiss franc, blue line). While the price has increased over the sample it is quite volatile. One does not want to need to cash out of an oil account at the wrong time.

Furthermore, storing oil is not free: the bilur has a fee of 3.65 percent per year to cover storage costs. This is far from a cheap deal, and it we take the value of savings put in oil net of this fee (the red line in the chart) we end up with 9.9 Swiss franc per barel, which is less than the initial investment of 14.45 franc. A good old banknote under the mattress would have been a better investment.

Money is a bubble (and that’s how it’s supposed to be)

Any currency preserves value only if we can in the end exchange it for goods and services. The keystone of money – and any means of exchange – is the agreement by buyers and seller to use it.

Money is thus a social convention, and its value follows from this agreement and not from any intrinsic feature. In technical terms, money is a bubble, that is an asset which has value only because we give it some (no need to worry as the bubble is not a speculative one as long as money is enforced in law).

The same applies to any physical support: the value of gold for instance is well above its usefulness in jewelry or dentistry. Of course gold has had an important role historically. But this is because if replaced weak institutions, and did not do so perfectly as the gold standard put a straightjacket on economic policy.

Independent central banks with a clear mandate of price stability are a more efficient institution. It’s true that they are only as solid as the underlying political will. But this is so for all laws.